Lincoln is an investor and content marketer. He has worked for financial advisors, institutional investors, and a publicly-traded fintech company. Lincoln holds degrees in Finance, Economics, and Accounting.

Earning a yummy yield on savings has never been so simple.

With the explosion of digital-only banks and high-yield savings accounts, you can get a decent chunk of change without fretting about market volatility.

Sounds too good to be true, right? Well, in some cases, the fine print can put a dent in this strategy.

However, there are many legit ways to earn from a nearly 5% interest savings account—you just have to know where to look (and what to look for).

Reviewing the best high-interest savings accounts will put you in a stronger position to make low-risk interest.

Quick context for May 2026: the Federal Reserve trimmed its benchmark rate three times in late 2025 and has held steady through the first half of 2026, with the next rate decision scheduled for June 17, 2026. That means HYSA rates have eased off the highs we saw in 2023–2024, but the top accounts are still paying around 4% APY — roughly 10x the national average of 0.38%.

Rates current as of publication. APYs are variable and may change without notice — check each bank’s site for the latest figures before opening an account.

What bank has the highest interest rate?

On paper, Varo offers the most attractive APY with a 5% interest savings account, but that’s not technically the best deal.

You see, Varo only pays the headline 5% APY on the first $5,000 — and only if you meet a couple of monthly requirements. Every dollar above $5,000 (and your entire balance if you miss the requirements) earns 2.50% APY instead. So if you plan to park more than $5,000 in savings, Varo’s offering won’t give you the most bang (or “bank”) for your buck.

CIT Bank, by contrast, currently pays 3.75% APY on balances of $5,000 or more through its Platinum Savings account, with a limited-time promotional boost to 4.10% APY for the first six months when new customers use the promo code CITBOOST at sign-up. For a saver with $10,000+ sitting in savings, CIT delivers a better overall return than Varo’s tiered structure.

That being said, keep in mind that APYs on savings accounts are constantly shifting. Unlike CDs, you won’t get a locked-in rate for however long you keep your money in one of these accounts.

Therefore, it’s best to keep an eye on whichever bank you start out with and shop around for the most competitive rates.

For scannable reference, here’s a table showing the highest APY savings accounts, along with the actual total interest you would earn if you deposited $10,000:

Savings Account | APY | Total Interest Earned Annually | Learn more |

|---|---|---|---|

Up to 4.35% on accounts over $5,000 | $375 (standard) or – $393 (with 6-mo promo blend) | ||

4.6% | $460 | ||

4.25% (temporary boost to 4.75% using this link) | $475 | ||

4.2% | $420 | ||

5% on the first $5,000; 2.50% on balances after that | $375 |

Pros and cons of a 5% interest savings account

With close to a 5% kickback plus FDIC insurance, there isn’t much to complain about.

It’s true; high-yield savings accounts are a sweet deal for conservative and passive investors. However, there are a few potential downsides that might dampen your “money dance.”

Pros:

- Cash accessibility: Unlike bonds, CDs, or fixed-income investments, a high-yield savings account lets you withdraw your money without paying penalties, making it an extremely liquid option.

- Low deposit requirements: Many of the best high-interest savings accounts don’t have minimum account requirements. Plus, even those that do have these minimums often require low amounts.

- Accessible and user-friendly: Many companies offering high-yield savings accounts are digital-first banks or platforms, making them super simple to install and use on laptops, tablets, and smartphones.

Cons:

- May have special account requirements: Some high-interest savings accounts have sneaky requirements — like making constant direct deposits or using products like debit cards — to unlock the holy grail of APYs.

- Sometimes includes interest caps: Some 5% APY savings accounts cap the maximum interest rate at a certain amount before offering a lower rate on the remaining funds.

- Variable APYs: High-interest savings accounts aren’t fixed-rate products. Expect some fluctuation in your monthly earnings, especially around FOMC meetings — top HYSA rates have already eased from 5%+ in 2023–2024 down to the 4% range in 2026 as the Fed has cut rates.

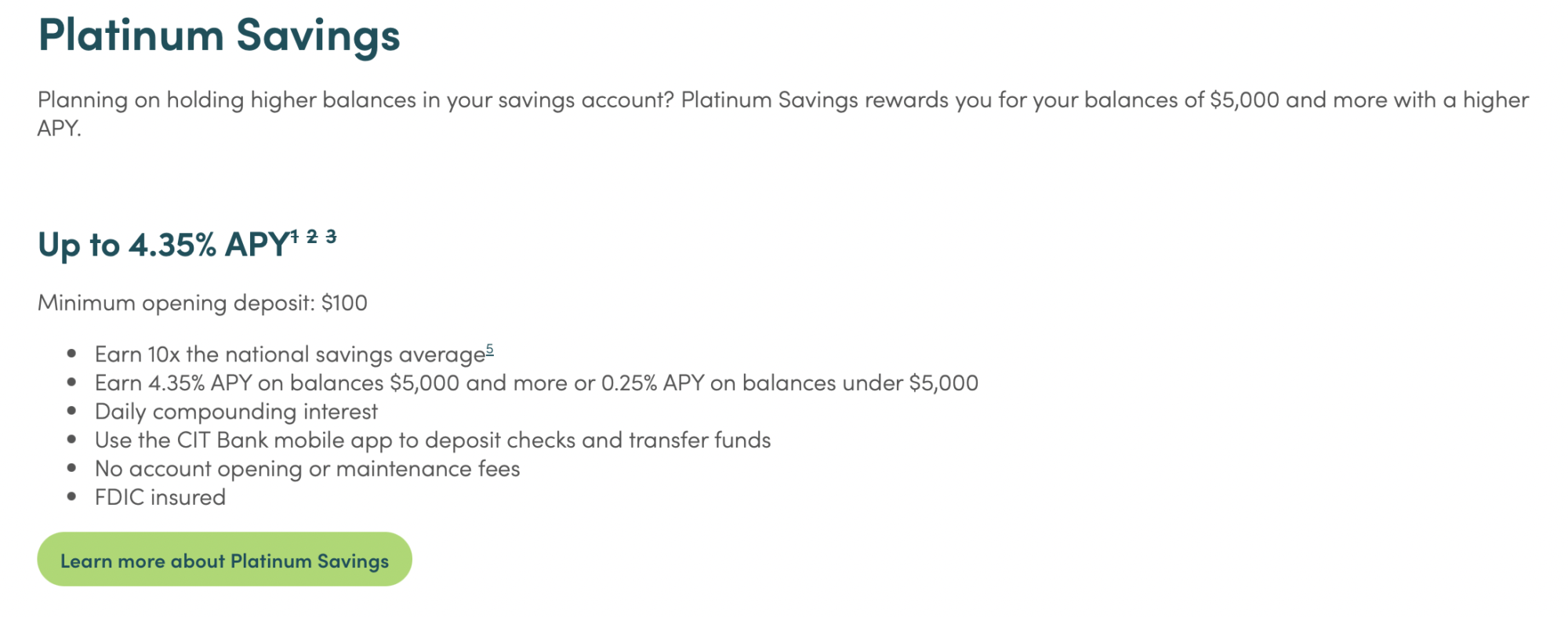

1. CIT Bank Platinum Savings

- Overall rating: ⭐️⭐️⭐️⭐️⭐️

- Account minimum: $100 / $5,000 to earn best APY

- APY: 3.75% standard (up to 4.10% with CITBOOST promo for new customers)

- Annual interest earned on $10,000: $375 standard ($410 with promo for first 6 months)

- Fees: None

If you plan to store at least $5,000 in savings, CIT Bank’s Platinum Savings is one of the best APY savings accounts you can open right now.

This FDIC-insured, online-only bank currently pays 3.75% APY on balances of $5,000 or more, with daily compounding and zero monthly fees. New customers can unlock a 0.35% promotional boost — bringing the APY to 4.10% for the first six months — by entering the promo code CITBOOST at sign-up. No direct deposit requirements, no spending minimums, just the code.

As you might’ve guessed, the catch is the $5,000 threshold. Any account below that figure drops to a much less exciting 0.25% APY. So this one isn’t a great fit for sub-$5,000 balances, but it’s hard to beat for larger long-term savings.

Pros

- Strong rate on balances of $5,000+, with a current 4.10% promotional boost for new customers

- No account opening or maintenance fees.

- Daily compounding interest.

Cons

- APY drops to 0.25% for sub-$5,000 accounts

- No access to trading services found on some other savings platforms.

2. Public

- Overall rating: ⭐️⭐️⭐️⭐️

- Account minimum: $0

- APY: 3.30%

- Annual interest earned on $10,000: $330 (simple interest); approximately $335 with daily compounding

- Fees: None

Public.com is a financial “super app” that offers a lot on one platform, including trading for assets like stocks, ETFs, bonds, Treasuries, and crypto.

Public’s High-Yield Cash Account currently pays 3.30% APY — a step down from the headline rates of 2024, but Public makes up the difference in two ways most banks can’t match. First, your cash is swept across 20 partner banks, giving you up to $5 million in combined FDIC coverage (20x the standard $250K limit at a single bank). Second, there are no fees, no subscription tiers, no minimum balance, and no maximum cap — just unlimited transfers and withdrawals.

If you’re a larger saver who’s bumped up against single-bank FDIC limits, that $5M coverage is genuinely hard to find elsewhere on this list. And if you’re already using Public to trade stocks, ETFs, or crypto, keeping your cash on the same platform makes for a tidy setup.

Pros

- No minimums or maximums.

- $5 million FDIC coverage across 20 partner banks (20x the standard limit)

- Zero fees, no subscription, no minimum or maximum balance

- Unlimited transfers and withdrawals

- Access to other assets on Public.com, including stocks, ETFs, bonds, Treasuries, and crypto.

Cons

- No phone support.

- Works with affiliate banks rather than a standalone bank.

- Shortest track record on this list (founded in 2019).

3. M1 Finance – High Yield Cash Account

- Overall rating: ⭐️⭐️⭐️⭐️⭐️

- Account minimum: None

- APY: 4.25% standard (boost rates may apply via affiliate link — verify current promotional terms)

- Actual annual interest earned on $10,000: $425 at 4.25%

- Fees: $3/month for accounts under $10,000; no monthly fee for accounts above $10,000

With M1 Finance, you can earn up to 4.25% APY on your cash without any fees, provided you deposit at least $10,000.

While you’ll still get the 4.25% on accounts under $10,000, you’ll have to subtract a $3 monthly fee from your interest earnings.

(FYI: M1 Finance used to make users sign up for a special “M1 Plus membership” to get this savings account at $10 per month.)

Beyond earning a decent reward on your savings, the M1 Finance app has many other investment-friendly features if you’re looking for a more active way to invest your money.

In fact, M1 brands itself as a “Finance Super App,” so be sure to take a peek at all of these superpowers (like stocks, ETFs, and options).

Pros

- Access to many other financial products, including stocks, ETFs, and crypto.

- No minimum deposit required, and no fees for over $10,000.

- Offers features like custodial accounts, IRAs, and personal loans.

Cons

- A relatively high minimum to qualify for no fees.

- $3 per month fee for under $10,000.

4. Empower Personal Cash

- Overall rating: ⭐️⭐️⭐️⭐️

- Account minimum: $0

- APY: 3.00% standard (up to 3.30% with qualifying $750+ monthly direct deposits)

- Annual interest earned on $10,000: $300 at standard rate ($330 at premium rate)

- Fees: None

Empower has been around the investment and retirement planning game for over a century, and it continues to innovate to stay competitive in the financial planning landscape.

Empower Personal Cash is the company’s high-yield cash management account — a hybrid that blends checking-style access with savings-style returns. It currently pays 3.00% APY on all balances with no minimums and no fees, and you can boost that to 3.30% APY by setting up qualifying direct deposits of $750 or more per month from the same source.

One of Empower’s standout perks is the FDIC coverage: your cash is swept across a network of partner banks via UMB Bank, giving you up to $5 million in aggregate FDIC insurance (20x the standard $250K limit at any single institution). That’s genuinely useful for larger savers who’ve outgrown single-bank coverage.

Just note that Empower isn’t a bank itself — it’s a cash management platform working with UMB and a network of program banks. The APY is also below some competitors on this list, so it’s most compelling for Empower’s existing investment customers who want a tidy place to keep uninvested cash, or for savers prioritizing the $5M FDIC ceiling over the absolute top rate.

Pros

- Zero minimums, no account opening cost

- $5 million aggregate FDIC insurance through partner bank network

- Long-established brand (Empower has 110+ years of financial services history)

- Up to $100,000 daily withdrawal limit with unlimited transfers

Cons

- Standard 3.00% APY is below several competitors on this list

- The 3.30% premium tier requires $750+ in qualifying monthly direct deposits

- Not a direct bank — operates as a cash management program through UMB Bank

- No physical cash deposits, no debit card, no check writing

5. Varo

- Overall rating: ⭐️⭐️⭐️⭐️

- Account minimum: $0

- APY: Up to 5%

- Actual annual interest earned on $10,000: $400

- Fees: None

With Varo’s savings account, your base rate starts at 2.50% APY the moment you open the account. But here’s where it gets interesting — you can supercharge that to 5.00% APY on the first $5,000 in your balance, if you meet two simple monthly requirements.

The deal: receive at least $1,000 in qualifying direct deposits during the month, and end the month with a positive balance across your Varo accounts. Hit both, and the 5.00% APY kicks in the following month. Any balance above $5,000 continues to earn the standard 2.50% APY — still about 6x the national average of 0.38%.

Pros

- Varo doesn’t charge any fees.

- Offers a combination of 5% and 3% APY for minimal effort with Stacks 5.00% and 2.50% APY tiers with no monthly fees and no minimum balance

- Ideal for a moderate savings account (below $5,000).

Cons

- You need consistent $1,000 direct deposits to qualify for 5% APY.

- It’s not perfect for accounts larger than $5,000.

How to Find More Money to Save

A high-yield savings account only helps if money is actually going into it.

Rocket Money helps free up extra cash by tracking recurring subscriptions and negotiating phone, cable, and electric bills on your behalf. Premium users can also have Rocket Money submit cancellation requests on their behalf.

For many people, cutting a few forgotten charges is enough to finally build real savings momentum.

Rocket Money is free to download. Premium plans run $7–$14/month with a 7-day free trial.

Final Word: The Highest APY Savings Account Doesn’t Actually Offer 5% Interest Rate

The highest APY savings accounts aren’t usually the ones with the highest interest rates unless you maintain a balance of only a few thousand dollars.

This is because these banks typically limit the 5% interest rate to small balances and then drastically reduce interest rates on additional cash. So for balances exceeding $5,000, options like CIT Bank Platinum Savings or M1 Finance are your better bet.

There’s still money to be made with these 5% interest savings accounts — particularly if you’re willing to split your cash between accounts. Park the bulk of your savings in an uncapped account with a strong base rate, and keep a smaller amount in a tiered 5% account like Varo to capture the higher rate where it actually applies.

.

FAQs:

Are there any savings accounts that pay 5% interest?

Yes — but typically only on capped balances and only when you meet qualifying requirements. Varo, for example, pays 5.00% APY on the first $5,000 when you receive $1,000+ in monthly direct deposits and keep your accounts positive; balances above $5,000 earn 2.50% APY.

What bank currently has the highest savings interest rate?

Top HYSA rates in 2026 sit around 4%–4.10% APY, with CIT Bank Platinum Savings offering a promotional 4.10% APY for the first six months for new customers (using promo code CITBOOST) on balances of $5,000+. Rates change frequently — always check the bank's site for the current figure.

Are there 6% or 7% interest accounts?

Not from FDIC-insured banks in the current rate environment — anything advertising 6%+ on a standard savings account should be treated as a red flag. Some credit unions and rewards checking accounts offer 5%+ on capped balances with specific qualifying requirements, but those aren't standard HYSAs.

Is 1% APY on a savings account good?

It's better than the 0.38% national average, but well below what top high-yield savings accounts pay in 2026. Most competitive HYSAs are currently offering 3.5%–4.10% APY with no minimum balance — meaning a 1% rate is leaving real money on the table.

Where to Invest $1,000 Right Now?

Did you know that stocks rated as "Buy" by the Top Analysts in WallStreetZen's database beat the S&P500 by 98.4% last year?

Our August report reveals the 3 "Strong Buy" stocks that market-beating analysts predict will outperform over the next year.