Jessie Moore has been writing professionally for nearly two decades; for the past seven years, she's focused on writing, ghostwriting, and editing in the finance space. She is a Today Show and Publisher's Weekly-featured author who has written or ghostwritten 10+ books on a wide variety of topics, ranging from day trading to unicorns to plant care.

Key Points:

- Dave’s revenue surged 63% year-over-year to $150.8 million in Q3 2025, with full-year adjusted EBITDA growing more than 160%.

- The company’s proprietary CashAI v5.5 underwriting engine is driving stronger credit performance, pushing its 28-day delinquency rate to an expected range of 1.95% to 2.00% in Q4.

- Dave is preparing to launch a buy-now, pay-later product in early 2026, targeting the roughly 60% of its 13 million members already using competing BNPL services.

Dave (DAVE) has had a remarkable run. Shares of the Los Angeles-based neobank have doubled over the past year, and the company keeps finding new ways to justify the rally.

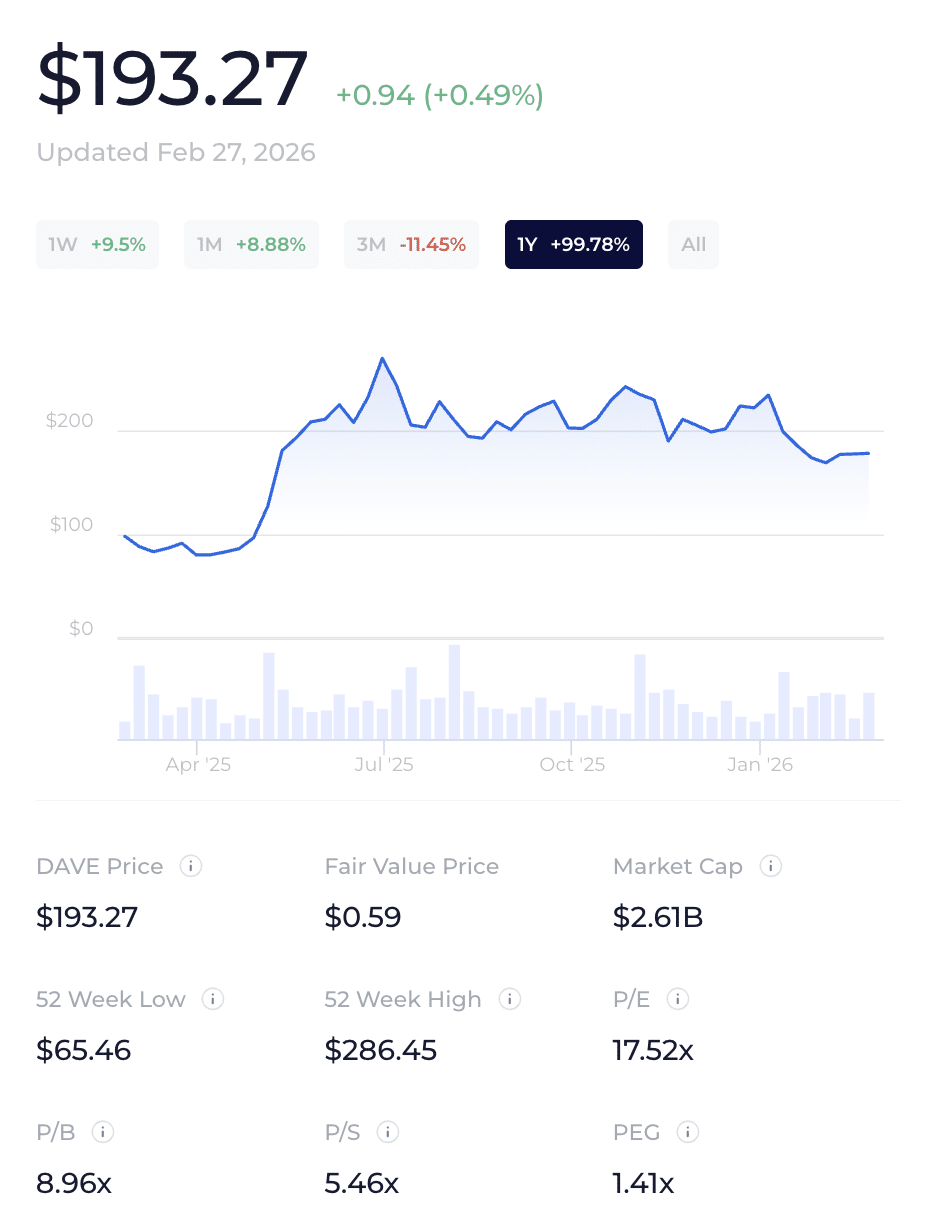

After closing out 2025 with its strongest year on record, Dave looks like more than just a momentum story. Valued at a market cap of $2.60 billion, Dave stock is still down almost 60% from all-time highs.

The fundamentals are getting better in almost every direction. Revenue is surging. Profits are expanding rapidly. And management is laying out a credible case for continued growth in 2026 and beyond.

Here’s a closer look at what’s driving DAVE stock and what comes next.

Dave’s Revenue and Profit Growth Have Been Explosive

Dave’s third-quarter 2025 results were a clear signal that something real is happening here.

- Revenue jumped 63% year-over-year to $150.8 million.

- Monthly transacting members, the company’s key user metric, rose 17% to 2.77 million.

- And the company generated $58.7 million in adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization), good for a nearly 40% EBITDA margin.

That margin matters because it means Dave is not just growing. It’s growing profitably.

Then came the preliminary fourth-quarter results, released in early February. Dave said it closed out 2025 with a third consecutive quarter of 60%-plus revenue growth.

More importantly, full-year adjusted EBITDA grew by more than 160%nearly three times the company’s revenue growth rate. That kind of operating leverage is rare, and investors have noticed.

“Full-year Adjusted EBITDA grew over 160%, nearly three times our revenue growth rate,” Dave CEO Jason Wilk said in a company statement.

“A direct result of strengthening unit economics and deepening member relationships while maintaining our discipline on fixed costs.”

What Dave Does and Why It’s Working

Dave launched in 2017 with a simple mission: give everyday Americans access to the financial tools that big banks often don’t offer.

Its flagship product is ExtraCash, a short-term cash advance that helps members bridge the gap between paychecks.

Think of it like an emergency cushion. Members connect their bank account, Dave’s artificial intelligence-powered underwriting engine evaluates their cash flow, and the company decides whether and how much to advance.

The average advance lasts about 11 days. That’s a very short loan. But that brevity is actually one of Dave’s biggest competitive advantages.

Because the loans turn over so quickly, Dave can see almost immediately whether its underwriting decisions are working.

While traditional banks might wait a year or more to find out, Dave gets feedback in weeks. That speed allows the company to constantly adjust and improve its model.

Earlier in 2025, Dave overhauled its pricing, replacing an optional fee structure with a flat 5% fee. The change drove higher revenue retention and gave the company room to offer larger advances.

Yes, that led to slightly higher loss rates, but the increased revenue more than offset those losses. Net monetization per transaction hit all-time highs in both the second and third quarters of 2025.

That’s exactly the kind of trade-off a well-run financial company should be making.

CashAI Is Dave’s Secret Weapon

The engine behind all of this is CashAI, Dave’s proprietary artificial intelligence underwriting model.

The latest version, CashAI v5.5, was rolled out in late Q3 2025 and uses nearly twice as many AI-driven variables as its predecessor. The results have been encouraging. The company’s 28-day delinquency rate improved from 2.33% in Q3 to an expected range of 1.95% to 2.00% in Q4.

For context, that delinquency metric measures the percentage of advances from a given month that remain unpaid 28 days after the month ends.

Seeing that rate fall while originations are growing nearly 50% year-over-year is a meaningful signal.

“Credit is an input to our model, not an output,” Wilk said on the Q3 earnings call. “The company is very much in control over loss rates.”

Is Dave a BNPL Stock?

Dave isn’t stopping with ExtraCash.

The company has been quietly building a buy-now, pay-later product, and management says internal employee testing is already underway. Customer pilots are expected to begin in the first quarter of 2026.

The opportunity is significant. About 60% of Dave’s 13 million members are already using some form of buy now, pay later through other providers.

Dave currently captures zero of that market. If it can convert even a portion of those users to a competitive product—backed by CashAI’s cash flow underwriting—that could be a meaningful new revenue stream.

Most buy-now, pay-later providers rely on traditional credit bureau data to assess customers.

Dave would be the only player in the space using real-time bank transaction data, which gives it a structural edge in approving more people and setting better limits.

What is the DAVE Stock Price Target?

Analysts tracking DAVE stock forecast revenue to increase from $552 million in 2025 to $748 million in 2027. In this period, free cash flow is forecast to expand from $270 million to $369 million.

If DAVE stock is priced at 12x forward FCF, it could gain close to 70% over the next 12 months.

DAVE has a Zen rating of “B” and stocks in this category have generated an average annual return of 19.88%.

Is Dave Stock a Good Buy Right Now?

There’s also a potential macro catalyst that management flagged in its preliminary fourth-quarter update.

Policymakers have floated a proposal to cap credit card interest rates at 10%. If that happens, some industry insiders suggest credit card access could shrink by as much as 80% for non-prime and subprime consumers.

That’s a massive population, and they’d still need access to liquidity.

“The need for liquidity does not disappear,” Wilk said. “It shifts to alternatives that better match a customer’s needs and ability to repay.”

That framing is apt. Dave has spent years building a product for exactly the consumers who get squeezed out of the traditional banking system. If credit card access tightens, Dave could see demand accelerate sharply — without spending a dollar more on marketing.

For investors, the story here is straightforward. Dave is growing fast, its margins are widening, and it has multiple paths to keep that momentum going.

Where to Invest $1,000 Right Now?

Did you know that stocks rated as "Buy" by the Top Analysts in WallStreetZen's database beat the S&P500 by 98.4% last year?

Our March report reveals the 3 "Strong Buy" stocks that market-beating analysts predict will outperform over the next year.