Jessie Moore has been writing professionally for nearly two decades; for the past seven years, she's focused on writing, ghostwriting, and editing in the finance space. She is a Today Show and Publisher's Weekly-featured author who has written or ghostwritten 10+ books on a wide variety of topics, ranging from day trading to unicorns to plant care.

Astera Labs Key Points:

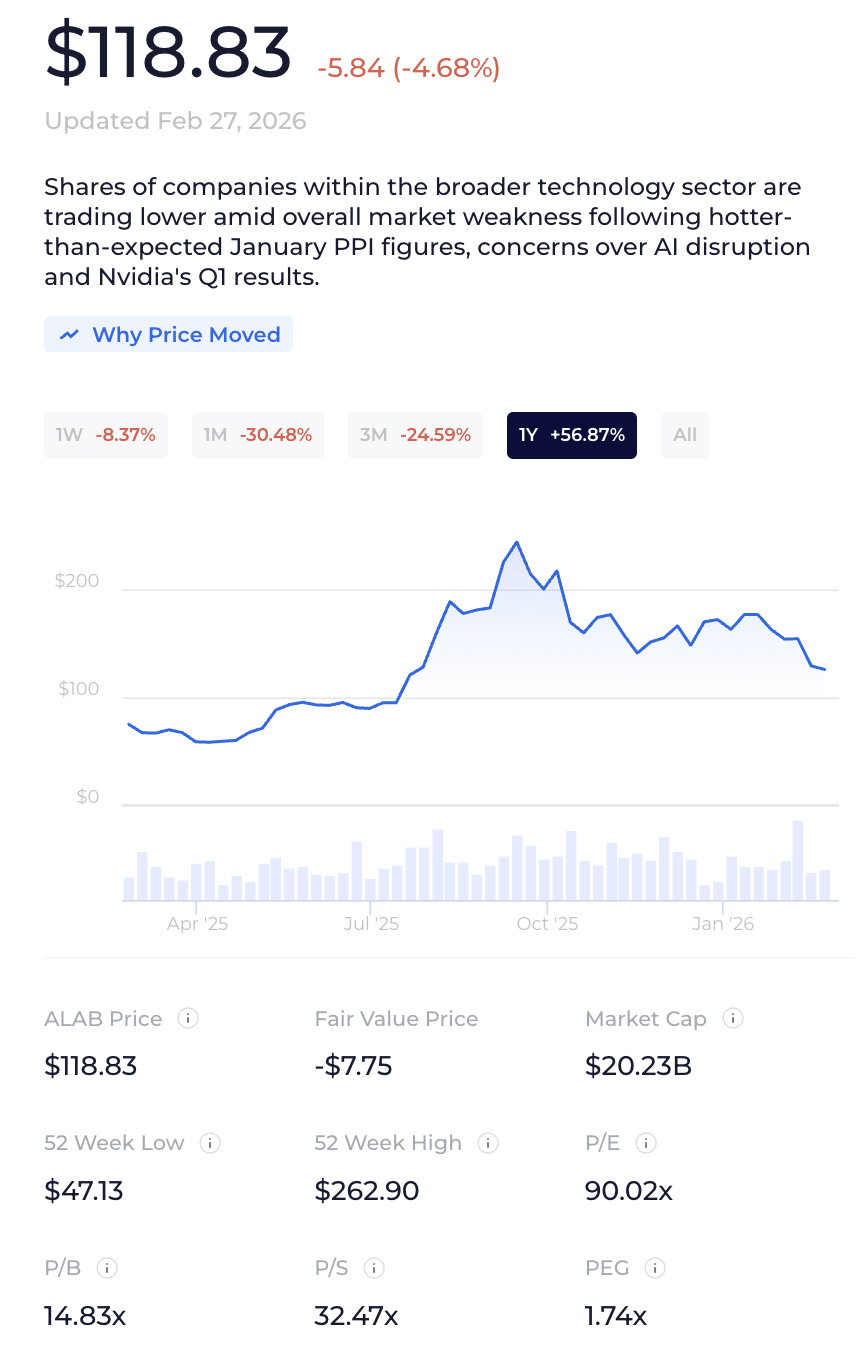

- Astera Labs posted full-year 2025 revenue of $852.5 million, up 115% year-over-year, with Q4 revenue of $270.6 million representing 92% growth from the prior-year period.

- Amazon signed a warrant agreement tied to up to $6.5 billion in product purchases from Astera, covering fabric switches, signal-conditioning solutions, and optical engines through 2033.

- Analysts project Astera’s revenue will nearly double to $1.85 billion by 2027, with free cash flow expected to reach $840 million by 2028, as demand for AI connectivity infrastructure accelerates.

Astera Labs (ALAB) recently made a big move to strengthen its position in the AI infrastructure race.

The San Jose-based chip company announced the establishment of a new advanced design center in Israel, a major expansion of its global engineering operations.

The timing isn’t accidental. Astera is sitting on a mountain of customer demand and needs the engineering firepower to keep up.

ALAB stock has been on a tear in the past year, and the numbers explain why. Full-year 2025 revenue hit $852.5 million, up 115% year-over-year.

For context, analysts now expect that figure to reach $1.35 billion in 2026 and nearly $1.85 billion by 2027, according to TIKR estimates.

Basically, Astera Labs is armed with a growing roster of the world’s biggest tech spenders knocking on its door.

What Astera Labs Does

Astera Labs makes the chips and software that connect the components inside massive AI data centers.

Think of it like the nervous system of a rack-scale AI system. Without reliable, high-speed connectivity between processors, memory, and networking gear, AI models can’t train or run efficiently.

Astera’s products fall into a few categories.

- Its Scorpio switches handle the traffic between AI accelerators.

- It’s Aries retimers extend the reach of signals across a server board or cable.

- Its Taurus products do the same for Ethernet connections.

- And its Leo products address the memory bottleneck that is increasingly slowing down AI inference workloads.

All four product lines are now generating meaningful revenue — and all four are growing.

Astera’s Q4 2025 results were impressive.

Revenue came in at $270.6 million, up 17% from the prior quarter and up 92% from the same period a year ago. Non-GAAP operating margins stood at a healthy 40.2%. ALAB stock closed the quarter with $1.19 billion in cash and marketable securities.

For Q1 2026, management guided revenue of $286 million to $297 million, another sequential jump of roughly 6-10%.

The growth isn’t tied to a single product or customer. It’s broad-based. Scorpio switches are ramping at multiple hyperscalers.

Aries retimers grew nearly 70% for the full year. Taurus revenue grew more than four times year-over-year. That kind of diversification is what separates durable businesses from one-hit wonders.

ALAB Stock and the Amazon Warrant Deal

Buried in the earnings release was a disclosure that deserves more attention.

Astera filed an 8-K revealing a warrant agreement with Amazon. Under the terms, Astera is issuing 3.3 million warrant shares to Amazon, tied to Amazon’s purchase of up to $6.5 billion of Astera’s products, including fabric switches, signal conditioning solutions, and optical engine products.

Amazon is locking in a long-term relationship with a company it clearly views as critical infrastructure.

“It demonstrates our strong relationship with Amazon,” outgoing CFO Mike Tate said on the call. “This is a follow-on warrant. We’ve had a previous warrant agreement in place.”

The warrant does create a noncash accounting charge, roughly 2 percentage points of gross margin pressure per quarter starting in Q2, but that’s a small price to pay for visibility into a multi-billion-dollar customer commitment.

The Israel Design Center Is About Keeping Pace

Back to the new design center. The facility in Israel will widen Astera’s capabilities. Astera is seeing customer requests come in faster than it can respond to them.

The Israel team will focus specifically on AI fabrics and high-bandwidth custom connectivity, areas where Astera is trying to expand from a position of strength.

The company also closed an acqui-hire transaction this quarter to quickly staff up the new center with experienced ASIC engineering talent.

“The time to invest is now,” President and COO Sanjay Gajendra said on the call. “This will help us as we think about the longer-term growth of the company.”

Operating expenses are stepping up as a result, from roughly $96 million in Q4 to a range of $112 million to $118 million in Q1.

But management’s argument is straightforward: the revenue opportunities presented by customers far outweigh the cost of pursuing them.

What is the Astera Labs Stock Price Target

The TIKR estimates tell an interesting story about where analysts expect this to go.

Revenue is projected to reach $2.35 billion by 2028, implying a compound annual growth rate of about 40%. Free cash flow is expected to grow from $281.8 million in 2025 to $840.2 million by 2028. Net income margins are projected to expand as well, reaching nearly 40% by 2028.

In the last 12 months, ALAB stock has been priced at 85x forward FCF on average. If this multiple normalizes to 50x, Astera Labs stock could surge 100% over the next two years.

Those are the kinds of numbers that attract serious long-term investors.

ALAB has a Zen Rating or “C” or “Hold”. Typically, the average annual stock returns for companies in this category is around 7.53%.

Astera still faces real risks. Operating expenses are rising fast and competition from larger peers such as Marvell, Broadcom, and others is intensifying.

But the company has something many competitors don’t: years of production experience, deep customer relationships, and a software-defined architecture that can adapt as the AI infrastructure market evolves.

The new Israel design center is one more bet that the opportunity ahead is bigger than almost anyone initially expected.

Where to Invest $1,000 Right Now?

Did you know that stocks rated as "Buy" by the Top Analysts in WallStreetZen's database beat the S&P500 by 98.4% last year?

Our July report reveals the 3 "Strong Buy" stocks that market-beating analysts predict will outperform over the next year.